The Australian luxury retail market is experiencing a significant upswing, with central business districts (CBDs) maintaining their status as prime locations for global luxury brands. According to a recent analysis by LeaseInfo, the demand for high-end retail space in CBDs such as Sydney, Melbourne, and Brisbane remains robust, reflecting a solid growth trajectory despite economic uncertainties.

Growing Demand for Global Luxury Brands

The influx of international luxury brands, including mandates from global brands including Audemars Piguet, Chaumet, Missoni, Patek Philippe, Goyard, Brunello Cucinelli, Pinko, and Gentle Monster, highlights the sector’s expansion. These brands have traditionally targeted flagship locations in Australia’s significant CBDs, drawn by the prestige and visibility these prime locations command.

Market Rental Escalations

LeaseInfo’s analysis of 100 transactions in the luxury goods sector (including jewellery and watches) over the past five years reveals substantial rental growth. In Brisbane, the current average net face rent sits at $3,325 per square metre, while Sydney commands a staggering

$9,350 per square metre. These figures represent rental escalations of 7.5% in Brisbane and 6.5% in Sydney over the past year, underscoring the high demand for premium retail spaces. The average lease duration is six years, slightly shorter than five years ago at 7.5 years. This contributes to higher occupancy costs ranging from 3-5% for prime luxury and 5- 7% for mid-tier luxury retailers. Store sizes have increased as luxury retailers command more giant footprints for their flagship locations. This often includes multi-floor retailing in CBDs due to the lack of premium ground-floor space.

Simon Fonteyn, Executive Director of LeaseInfo—Powered by FLNT—says the premium in CBD rents is luxury marketing rental. “This often comes out of the marketing budget of the luxury retailers P&L, rather than a pure rental expense and sometimes is even reflected as COGS, reflecting a top line adjustment,” he says.

Significant Differences Between CBD and Suburban Rents

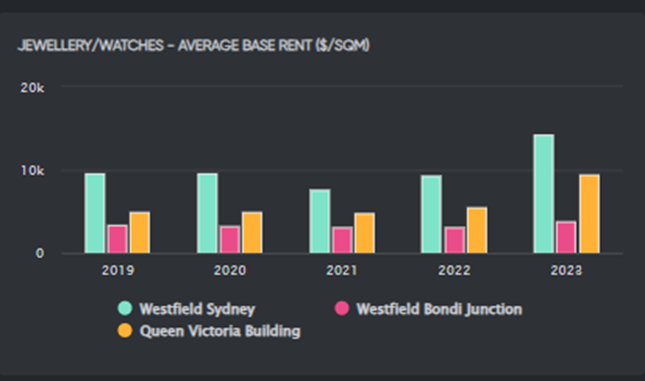

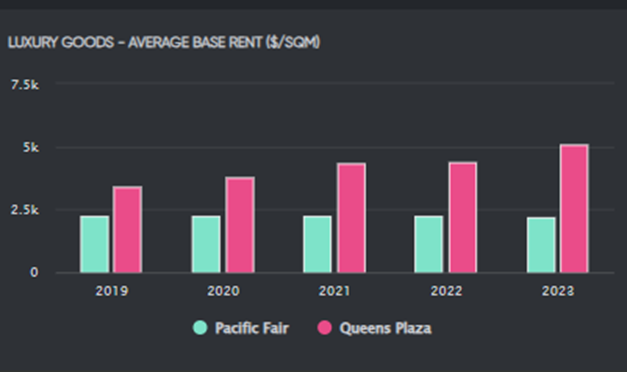

The pronounced disparity in rental rates between CBDs and luxury precincts in suburban shopping centres appears in Graph 1. For instance, the current passing rent for Westfield Sydney is $14,250 per square metre per annum net face, significantly higher than QVB’s $9,500 and Westfield Bondi Junction’s $3,800. In Brisbane, Queens Plaza’s luxury goods rent averages just under $5,100 per square metre per annum net face, compared to Pacific Fair’s $2,200, as shown in Graph 2.

Graph 1 Significant Rental Differences Between Suburban Malls for Luxury Retail, Watches and Jewellery and CBD Retail Shopping Centres

Source: Leaseinfo

Graph 2 – Luxury Rents in Pacific Fair vs Queens Plaza in Brisbane CBD Source: Leaseinfo

Source: Leaseinfo

Strategic Shift in Retailer Approaches

Luxury retailers have traditionally established flagship stores in CBDs to establish a brand presence. However, this trend is evolving, with some brands opting for suburban malls as their flagship locations. Notable examples include Tory Burch’s flagship store at Pacific Fair on the Gold Coast, Chadstone in Melbourne, and LVMH’s luxury jewellery brand Fred at Pacific Fair.

The Australian luxury retail market continues to expand, driven by solid demand and strategic expansion by global brands. The premium rents in CBDs reflect the high value placed on these prime locations, often subsidised by luxury retailers’ marketing budgets. However, this strategy is evolving, with the market entry point for some luxury retailers diverging into suburban luxury malls rather than traditional CBDs.